Featured articles

security

securityTo trust or not to trust? Romance scams, investment scams, and other online confidence tricks

4 min help & advice

help & adviceUnderstanding gambling and knowing when to walk away

3 min security

securityStaying safe when banking online

3 min security

securityScammers set their sights on older people

5 min security

securityGet smart about card fraud

5 min life

lifeFive money lessons to teach your children

4 min

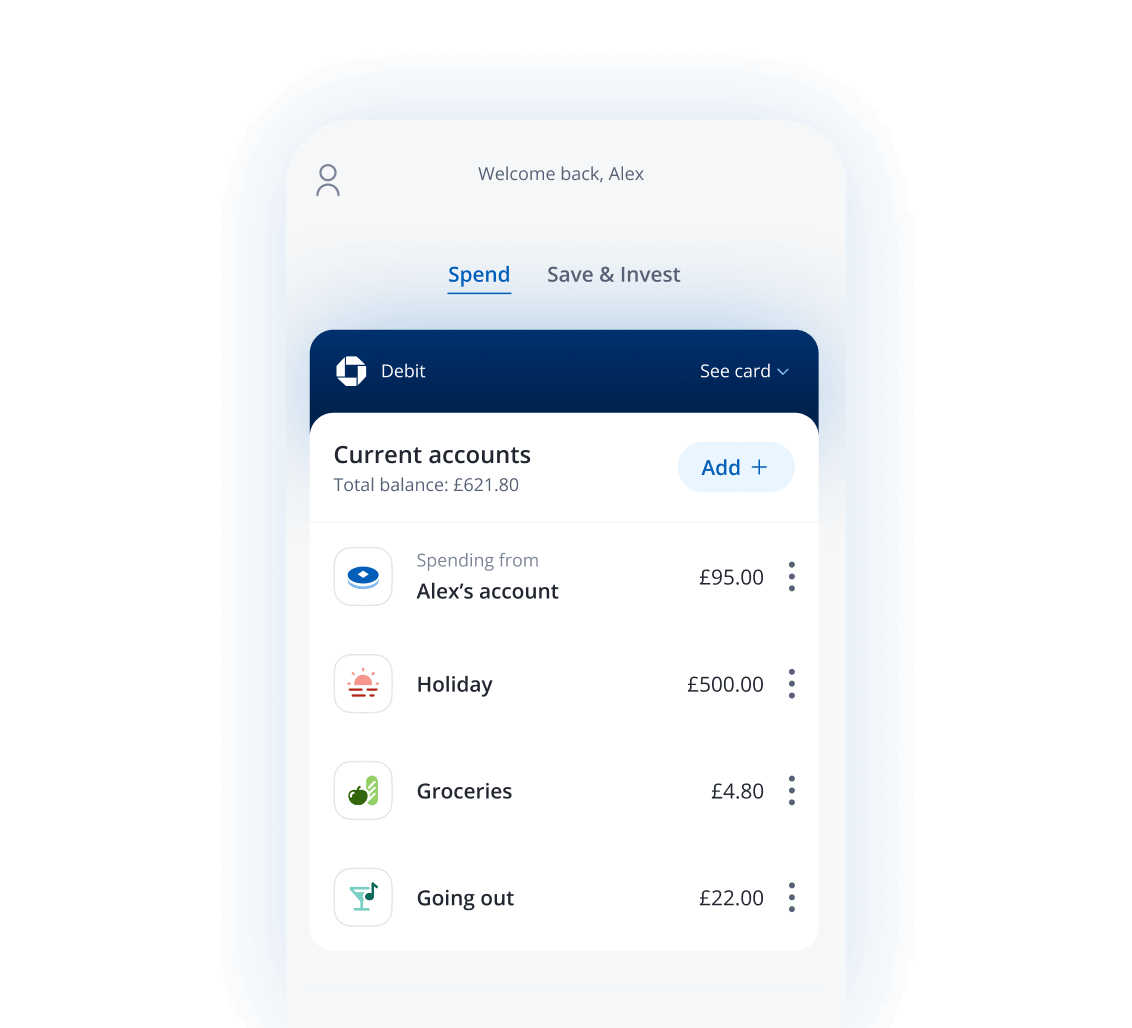

The new way to bank

Get to know the Chase current account. It's packed full of rewards and clever features that we think you'll love.

Explore the account